What Exactly is Fair Credit?

Fair credit refers to the federal law that prohibits lenders from charging higher interest rates to consumers who do not or cannot meet their financial obligations. In other words, borrowers with good credit scores are charged lower interest rates than borrowers with low credit scores.

Fair credit also prevents lenders from charging high fees or an unfair cancellation fee. That’s why when you have fair credit, you’re less likely to be turned down for a loan and will receive a lower interest rate than someone who doesn’t have fair credit.

What’s the Difference Between “Fair Credit” and “Good Credit”?

Fair credit is better than no credit, but it’s not quite as good as good credit. Having fair credit means that a borrower has a spotty financial history. The individual might have missed some payments on previous debts, but he or she is also able to make timely payments. Fair credit does not mean that the borrower has made all of his or her payments on time. It simply means he or she has had some financial mishaps in the past and has paid off those debts over time.

Is Fair Credit Better Than Bad Credit?

Yes, fair credit is better than bad credit . That’s because someone who has bad credit can have a high credit limit but is unable to utilize the full amount of that debt. In contrast, someone with fair credit will only receive the amount of credit that he or she has been approved for.

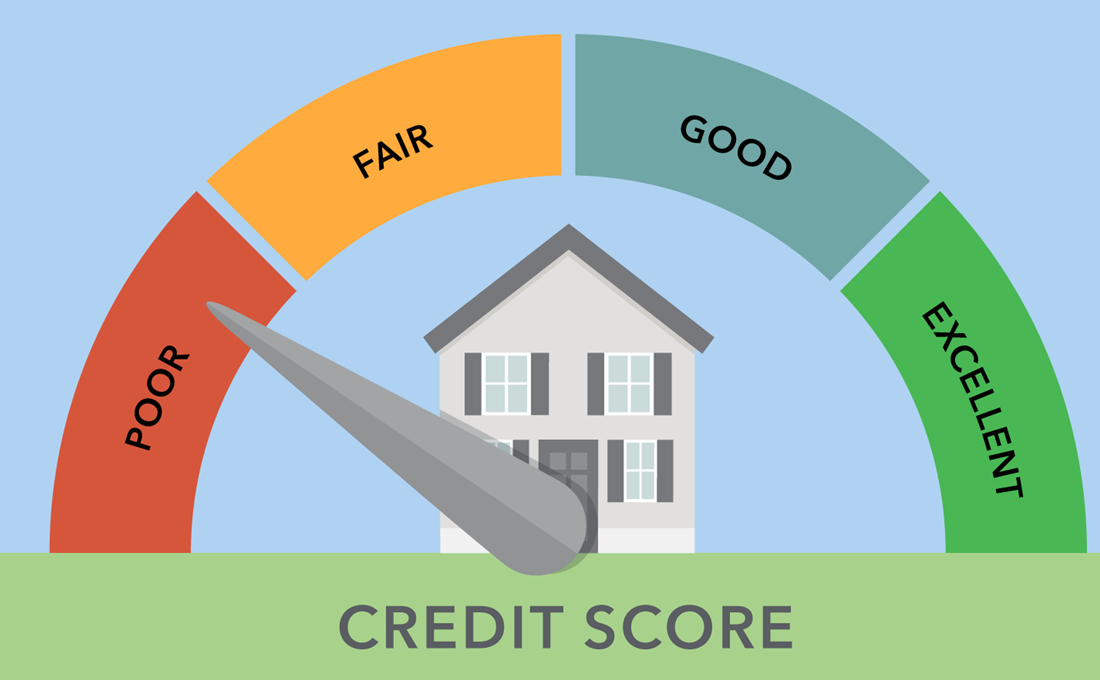

Do I Need Good Credit to Buy a House?

If you’re purchasing either a new home or your dream house, most lenders suggest that you are considered “credit worthy.” That means that you have demonstrated a history of making on-time payments in the past. That is because most mortgages require borrowers to make at least two, but sometimes three, consecutive monthly payments before a lender will approve the loan application.

What is a Credit Score? How Do I know if my Credit Score is Good or Bad?

Think of your credit score as a way for a lender to gauge your overall credit standing. It’s not so much about how much you have in debt, but, rather, how you handle that debt and the debts that you’ve taken on in the past. That’s why it’s important to always pay ALL of your bill on time. A good credit score means that you’ve been able to make all of your monthly payments and hasn’t had any delinquencies (late payments). Your FICO score is a way for lenders to calculate the strength of your financial history.